2022

Africa Tech

Venture

Capital

The African Tech sector was one of the very few, if not the only, VC markets to boast net growth funding in 2022. Globally, VC funding fell by 35% over the same period.

However, looking closely at the figures, this market was not left unscathed. We can see the slowdown began to seep into the African market in the first quarter of the year, with a 14% drop in activity compared to the last three months of 2021. Despite this, African start-ups still closed record funding in the first half of the year. In Q3, the slowdown really kicked in, with a year-on-year decrease in the number of deals and funding raised.

Still, looking back, we can only marvel at the dynamics of this market:

- The forces of growth driving the African Tech ecosystem were strong enough to compensate for the global crisis and leave us in 2022 with total numbers similar to those of 2021 (a year everybody will agree was an outlier).

- Early-stage activity was maintained with 600+ deals in Seed+ and Series A, building up the first stage of the rocket.

- A new milestone was set with more than 1,000 (1,149) unique investors investing in Africa, cementing the growing global interest in African start-ups. Even better, we saw more local investors dominating the charts at Seed and even at Series A stages.

The future, of course, is still unknown. Has the downturn impact reached its lowest point? What has the impact of the slowdown been on valuations? Will there be more consolidations?

Well, this report cannot answer these... yet. But what is reassuring are the strong fundamentals at play: a strong talent pool and resilient entrepreneurial environment, ubiquitous access and the digitization of key sectors.

Methodology & Data

Scope: We report on fundraising for African tech and digital start-ups, specifically venture capital equity and debt deals above US$200K.

Our numbers only include equity or debt rounds that amount to at least US$200K.

This means we focus on Late Seed (Seed+) to Growth stage equity & debt rounds. We omit Angel deals and smaller Seed deals below US$200K (numerous on the continent).

Example:

ProXalys’s round of US$150K funding in Senegal is not counted.

We only cover African start-ups. We define these as start-ups whose primary market (measured by operations and/or revenues) is in Africa. When these companies grow and go global, we will still count them as African companies.

Example:

KuCoin’s US$150M Series A is not counted as an African deal as, although the HQ is in Seychelles, the majority of the business is not derived from Africa.

We exclude everything else: grants, awards, prizes, Initial Coin Offerings (ICOs), non-equity/technical assistance, post-IPO, private investment in public equity (PIPE) and all M&A deals.

Examples:

- SWVL’s US$21.5M of PIPE from European Bank for Reconstruction and Development (“EBRD”), Agility, Luxor Capital Group and Chimera, announced in February 2022, is not counted.

- Thrive Agric’s US$1.75M grant from USAID in March 2022 is not counted.

Public vs non-public data

In this report, deals fall into three disclosure categories:

- Fully disclosed: these rounds are announced publicly or on professional platforms such as CrunchBase, Tracxn, PitchBook, etc. The major details of the round (Series, round size, investors) are also disclosed

- Partially disclosed: the existence of the rounds is disclosed but some details, especially round size, are not public. Participating investors are often disclosed. In this case we complete the information by reaching out to entrepreneurs and investors, promising confidentiality in exchange for including the data in our aggregate numbers, providing a more accurate overall picture.

- Confidential: these deals are not disclosed in the press or on platforms. We collect this data through engaging directly with investors and founders, again pledging confidentiality.

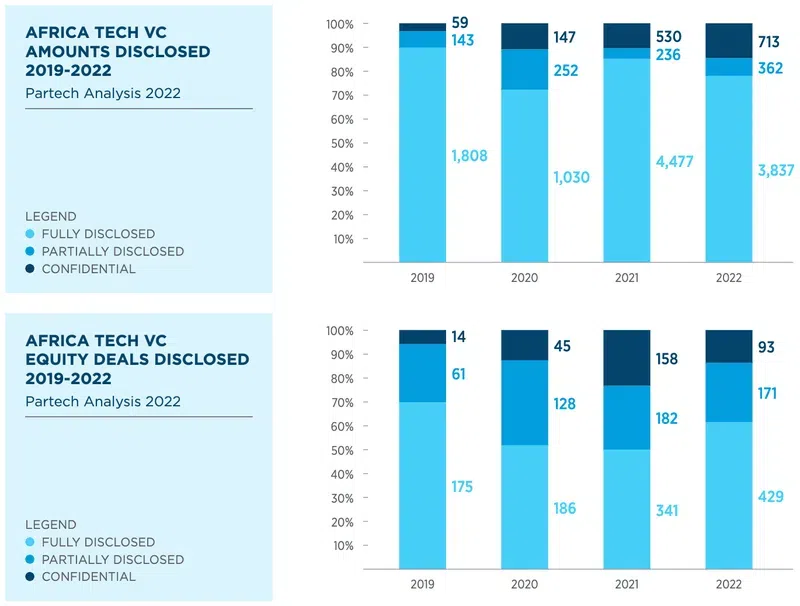

The charts below show aggregate metadata on the level of disclosure in our database entries:

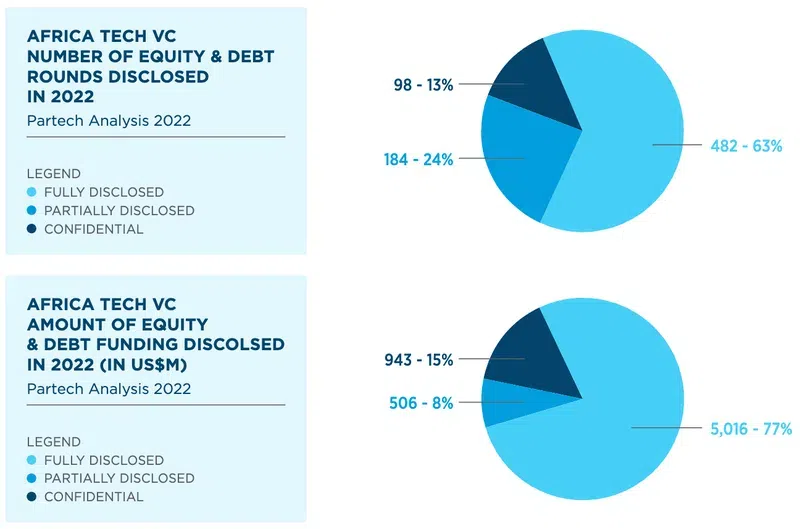

ALL DEALS

Looking at all equity and debt deals, the fully disclosed and partially disclosed deals represent 666 transactions out of 764 i.e. 87% of the total deal count and US$5.5B out of US$6.5B i.e. 84% of the total funding.

DISCLOSURE OF EQUITY DEALS

- Fully disclosed: 62% of deals were fully disclosed in 2022 (429 deals) - a significant increase from last year (50% in 2021). In terms of the amount of funding, this represents 78% of equity funding, vs 85% in 2021.

- Partially disclosed: this category reached 25% of deals in 2022 (171 deals), 2% less than in 2021. This represents 7% of equity funding vs 4% in 2021. Some founders and investors chose to disclose the existence of the rounds but kept the details such as round size confidential.

- Confidential: 13% of rounds were kept entirely confidential, a bit lower than 2021 (23%).

Most of the undisclosed and partially disclosed deals are Seed rounds (52%).

The fully publicly disclosed and partially disclosed deals represent 600 equity transactions out of 693 i.e. 87% of the total deal count (vs.77% in 2021) and account for US$4.2B i.e. 85% of the total equity funding (vs. 90% in 2021).

Summary of trends

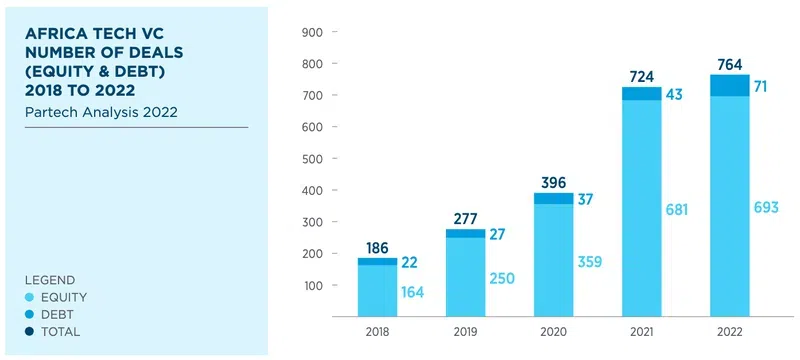

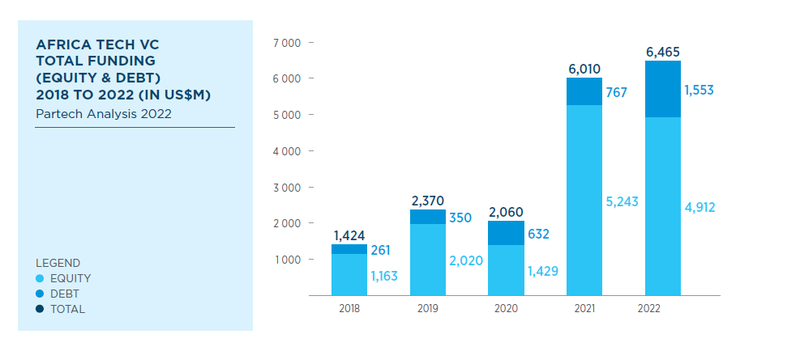

2022 was a particularly tumultuous year for the VC ecosystem, with global funding down -35% vs 20211. By comparison, Africa’s performance was fairly strong. Total funding (equity and debt) increased by 8% YoY to US$6.5B, and 764 deals were completed this year, representing a 6% increase YoY.

As 2021 was an outlier, we were watching for a correction in 2022 – and how any correction would affect the growth of the African ecosystem. It turns out the deeper growth trends, essential for Africa, were just strong enough to prevail.

One particular trend was key: African tech start-ups’ growing access to debt funding, which doubled in volume to US$1.5B, nearly a quarter of the total. It is another sign of growth and maturity for African start-ups.

Looking back over the last few years, we can see how the activity (deal counts) kept growing even during COVID in 2020 and the downturn of 2022. This points to a strong, early stage dealflow that builds on fundamentals (e.g. talent pool, entrepreneurial environment, ubiquitous access and digitization of key sectors etc.). The result has been a Compound Annual Growth Rate (CAGR) of 42% in activity since 2018.

A similar perspective on total funding amounts rather than deal counts still confirms this consistent growth. Despite a dip in 2020 during COVID, the ecosystem has not stopped growing, with a CAGR of 46% in funding volume since 2018: a 4.5x multiple over four years.

It’s too early to tell how this strong overall growth in the African tech ecosystem will hold as the downturn is still unfolding, but the sector’s strong fundamentals are likely to maintain the progress made in recent years.

Easily download the full report

SUBSCRIBE TO OUR NEWSLETTER