2021

Africa Tech

Venture

Capital

One could try to downplay the scale of this achievement. First, 2021 was a recovery year; after covid slowed investment in 2020, especially in the larger ticket category, accelerated activity was to be expected. Then, there is a rising tide that’s driving 2x growth in VC all over the world, not just in Africa. And finally it’s still a small market, growing fast in multiples yes, but absolute numbers are still relatively low.

But even taking all this into account, 3.6x growth in one year is a stunning success, shattering almost every record you’d care to measure.

It’s hard not to feel excited. A rapidly-expanding ecosystem, Africa tech VC hits new milestones every day. More and more teams are given fuel to test concepts, validate models and build scaling infrastructure, working to create new African champions.

As we break down the totals, some strong trends stand out: the Nigerian ecosystem is growing impressively large; Fintech is attracting an outsized portion of total funding; the average ticket size is inflating at all stages and there’s been an influx of new active investors.

All of this puts forward a new wave of questions around the value being created with this capital, the actual returns for investors and founders, the impact on local economies, etc. These are not questions this report can answer. What this report can do – and what we aim to do at Partech – is to contribute to the conversation. We feel fortunate to watch, chip in and cheer on Africa tech VC as its unique growth trajectory unfolds. By mapping its models, efficiency, scalability and impact, we hope to create a space for voices in the ecosystem to debate, explore options and turn this incredible momentum into even better outcomes.

The Partech Africa Team

Methodology & Data

Scope: Tech and digital VC equity and debt deals above $200K in African start-ups.

Our numbers only include equity rounds higher than $200K.

This ranges from late Seed (Seed+) to Growth stage equity rounds. Angel rounds and smaller Seed deals below $200K (and there are many of these) are omitted.

Example: Djamo’s $125K funding round from YC on March 21 is omitted.

We only cover African start-ups. We define these as companies whose primary market in terms of operations or revenues is in Africa, as opposed to companies who are HQ’d or incorporated in Africa. When these companies evolve to go global, they will still be considered by this report as African companies.

Example: Zipline’s $250M Series E is included as an African deal. The majority of its operations and revenue currently come from Africa and this round was advertised as enabling the company to double down on Nigeria and Ghana for new distribution centers while serving a new contract in the US.

For the first time, we’re covering debt deals. Over the last few years, debt has become an increasingly viable tool for African start-ups. This report adds a new section to share the data we’ve collected on this category, though the dataset is currently small as debt rounds do not receive the same publicity as equity rounds.

Everything else – including grants, awards, prizes, Initial Coin Offering (ICO), non-equity/technical assistance, post-IPO, PIPE and M&A deals – is omitted.

Examples: SWVL’s $35.5M of PIPE from Agility and Chimera Abu Dhabi announced in August 2021 is omitted. Mydawa’s $1.2M grant from the Bill & Melinda Gates Foundation in December 2021 is omitted.

Public vs non-public data

We categorize deals into three degrees of disclosure:

- Fully disclosed: these are rounds announced publicly and/or listed on platforms like CrunchBase, Tracxn, Pitchbook, etc. Major details of the round (series, round size, investors, etc.) are also available via public sources.

- Partially disclosed: these are rounds which are announced publicly, but the major details (especially round size) are withheld. In these cases, we complete the information by reaching out to entrepreneurs and investors confidentially and including the data in aggregates.

- Confidential: these are rounds which are not disclosed publicly. In these cases, we collect this data through direct and confidential engagement with investors and founders.

The charts below show aggregate metadata on the level of disclosure in our database entries:

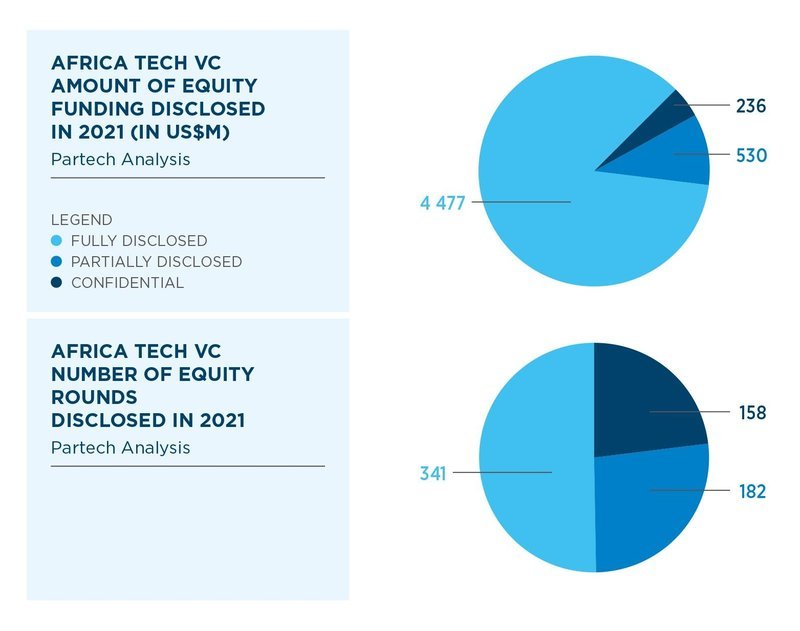

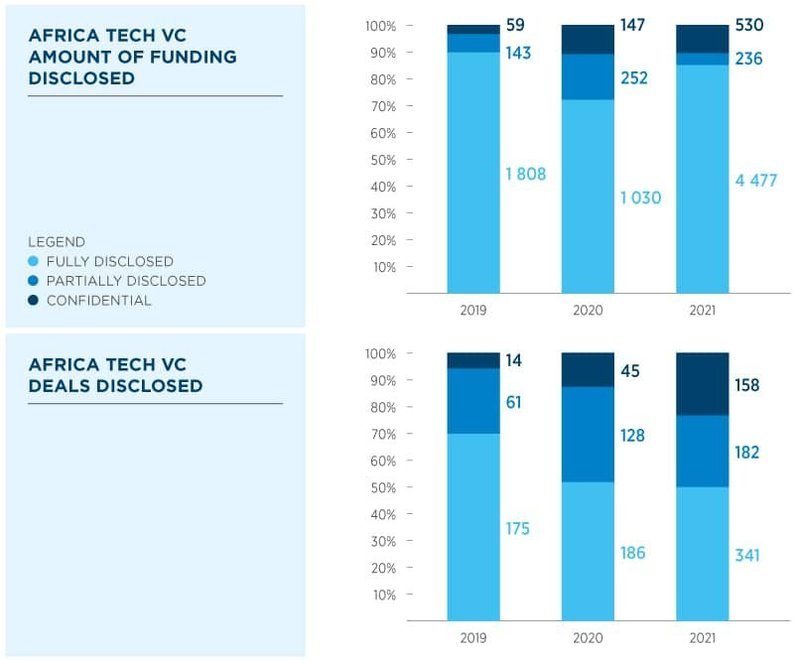

- Fully disclosed: 50% of deals were fully disclosed in 2021. This is consistent with last year’s numbers; 52% were fully disclosed in 2020. In terms of the proportion of total funding, fully disclosed deals represented 85% of funding in 2021, vs 72% in 2020.

- Partially disclosed: Only 27% of deals were partially disclosed in 2021, down from 36% in 2020. A number of founders and investors chose to disclose the existence of rounds but kept details such as round size confidential.

- Confidential: 23% of rounds were kept entirely confidential – a significant increase from 2020, when only 12% were confidential. Most of the undisclosed and partially disclosed deals were Seed rounds.

We’ve said before that we hope to see more transparency in the ecosystem, as we believe it drives positive impacts for both investors and entrepreneurs. Trends from 2019-2021 are disappointing in this regard: there has been no strong improvement in access to deal data, and no recovery from sharp drop in the number of fully disclosed deals in 2020. However, 85% of the total amount invested in 2021 was fully disclosed. This is an increase from 72% in 2020 and suggests that it is the growing number of seed rounds that are being kept confidential, as opposed to larger rounds.

Fully disclosed and partially disclosed rounds amounted to 523 equity transactions from 487 unique companies. This represents 77% of the total 681 rounds. This is a drop of 10% from 2020, but at $4.713B, accounts for 90% of total equity funding – exactly as in 2020.

Findings

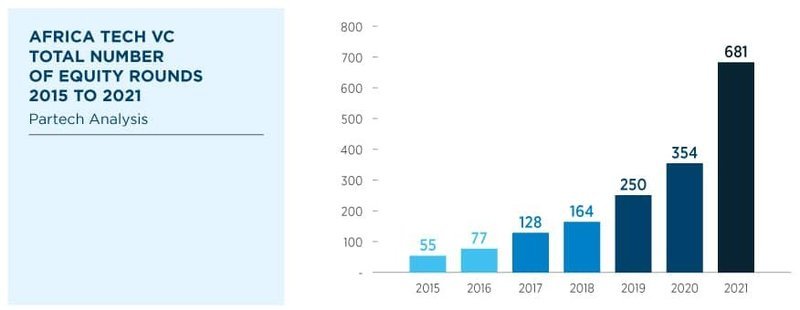

In 2021, we tracked a total of 681 equity rounds raised by 640 start-ups. This is a 92% increase in growth YoY compared to the 359 rounds raised by 347 start-ups in 2020.

Now in its sixth consecutive year of growth above and beyond expectations, we’re running out of superlatives to describe the African tech ecosystem.

681 equity rounds above $200K sets a new record. It indicates a super-active ecosystem, where almost 3 deals are closed every weekday.

The number of deals almost doubled, increasing by 92% YoY. This rate of growth makes African tech one of the fastest-growing ecosystems in the world. In 2021, it accelerated significantly, far outstrip- ping the past 6 years’ growth with a CAGR of 45%.

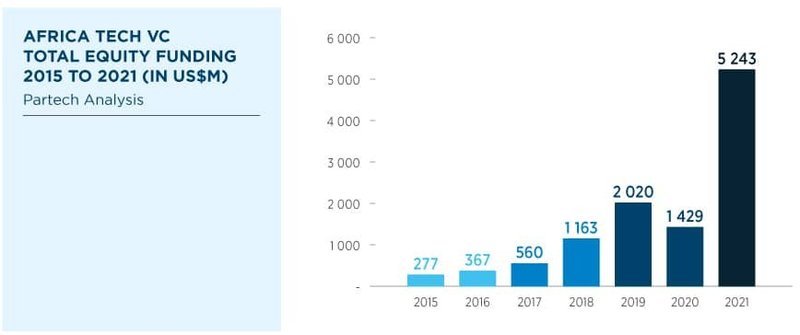

African start-ups raised a total of $5.2B equity funding in 2021. Up from $1.43B in 2020, this amounts to a+264% growth YoY.

In almost every year of reporting on Africa tech VC, a new record has been set. But $5.2B is a truly extraordinary milestone. It’s more than the total amount raised in the last 4 years combined.

2021 also saw the highest annual growth we’ve ever recorded, at +264% growth – 3.6x the previous year.

This puts African tech ahead of even LATAM, and indeed the rest of the world. It’s growing 3x faster than global VC investment, which reached $643B in 2021 at a growth rate of +92% YoY.

While there’s been an acceleration across all round brackets, total funding was driven by a re-surge in large rounds (i.e. rounds above $50M).

It’s clear that large rounds and Megadeals are back, after a complete pause in 2020. In 2020, there were only two rounds recorded above $50M; in 2021 there were 21, almost 10x more than the year before. Meanwhile, the amount invested in this bracket increased 21x.

A bounce back isn’t surprising after a year as quiet as 2020. But even compared against 2019, when these Megadeals first started gathering pace in Africa, 2021 saw more than double the number of Megadeals and 3x the amount invested.

As for large growth tickets, deal count in the $20M - $50M bracket doubled from 14 to 28 – again, a step up in the growth seen in previous years (36%).

Added together, all rounds equal to or higher than $20M accounted for more than 72% of total funding.

Easily download the full report

SUBSCRIBE TO OUR NEWSLETTER